The Quiet Revolution in African Financial Markets

- Adil Aboobakar, CFA

- Mar 14

- 3 min read

Something is shifting across Africa. It is not loud. It is not on the front pages. But for anyone who works with numbers for a living, it is unmistakable.

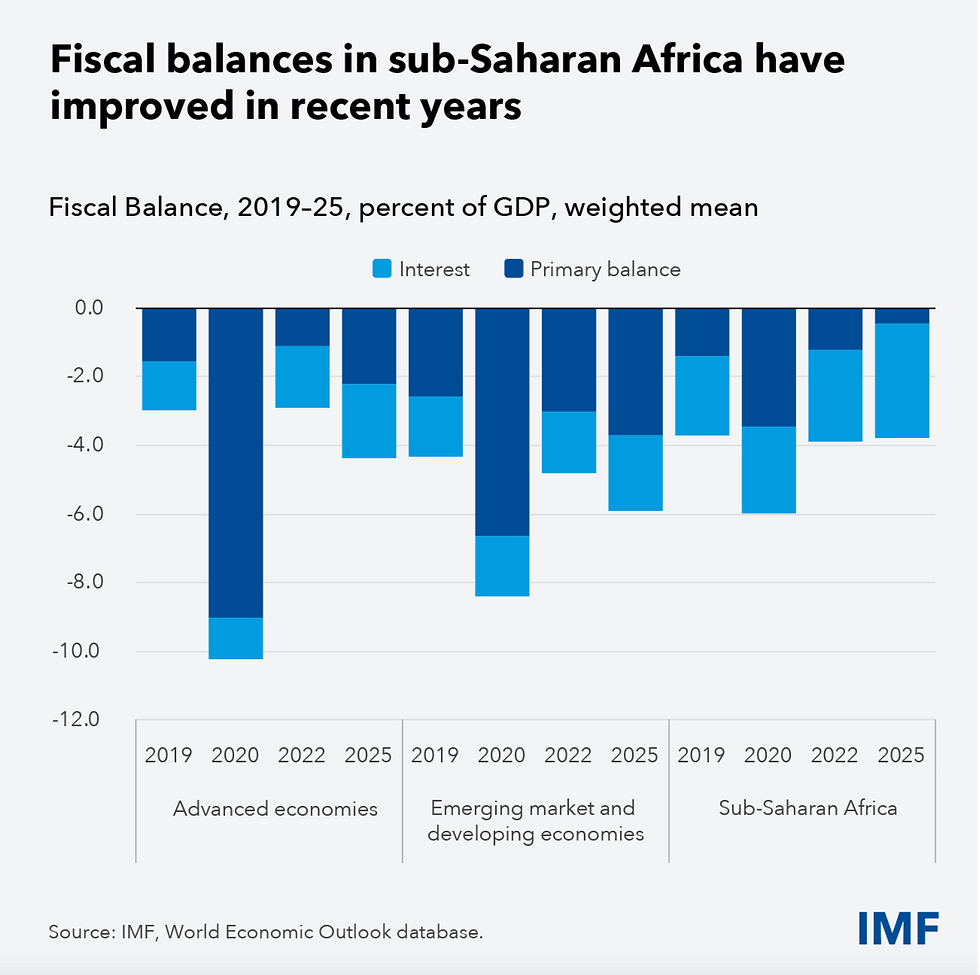

For most of the past three years, African economies have been fighting the same battle as the rest of the world — inflation, expensive capital, currencies under pressure, businesses holding their breath. That period is ending. According to the IMF's April 2026 Regional Economic Outlook, Sub-Saharan Africa grew 4.5% in 2025, the fastest rate in a decade. Median inflation has fallen to around 3.5%. Fiscal positions are the strongest they have been since before the pandemic. Central banks are cutting rates.

The cost of money is coming down. And that changes everything.

What falling rates actually mean.

Most people associate interest rate cuts with cheaper mortgages. The real effect runs deeper than that.

When analysts value a business, they use a discount rate — a number that reflects what money costs in the current environment. When that rate is high, future earnings are worth less today. Valuations compress. When it falls, the same business, generating the same revenues, the same profit, is worth materially more. Not because anything inside it changed. Because the world around it did.

This is the quiet part of the African story that almost nobody is discussing. Companies across the continent that were valued conservatively in 2023 and 2024 — under the full weight of tight monetary conditions — are sitting on valuations that no longer reflect their current reality. The macro environment has moved. The numbers have not caught up.

The stakes, honestly stated.

This is not a story without shadow.

The Middle East conflict has driven oil above $100 a barrel, and the ripple effects are real. The IMF is direct about what is at risk: fertilizer and shipping costs are rising, and a 20 percent spike in international food prices could push more than 20 million people across the continent into food insecurity, with 2 million children under the age of five facing acute malnutrition. The floods in Mozambique and Madagascar are a reminder that climate shocks do not wait for macro conditions to stabilise.

These are not footnotes. They are part of the same story.

The gains of the last three years were hard-won — the result of politically difficult reforms, tighter monetary discipline, and real institutional progress. Whether they hold depends on choices being made right now, by policymakers navigating pressures that have no clean answers.

Source: IMF Regional Economic Outlook: Sub-Saharan Africa, April 2026 — "Hard-Won Gains Under Pressure." imf.org

Why this moment matters.

Africa does not need to be the next Asia for this to be significant. Six of the ten fastest-growing economies in the world this year are African. Capital is beginning to notice. And the businesses that will benefit most from that attention are the ones that can demonstrate their value clearly — with credible numbers, prepared by people who understand both the opportunity and the risk.

A valuation produced at the peak of the rate cycle is a different document from one produced today. The inputs have changed. The conclusions will differ.

Most business owners across Mauritius and Africa do not yet know what their company is worth in this environment. That gap — between what the macro is saying and what owners actually know — is where the real quiet revolution is happening.

Comments