EVACO: A failure written in the filings

- Adil Aboobakar, CFA

- Jun 3

- 13 min read

Updated: Jun 4

Evaco Ltd was placed in receivership on 26 May 2026. Its own published accounts had been signalling distress for at least two years. What the numbers said, where the risk now sits, and what other developers, lenders, and a jurisdiction built on foreign property capital should take from it.

Executive summary

Early warning panel:

• Revenue dropping year-on-year across every comparable reporting window.

• Profit decoupled from cash.

• Finance cost climbing toward, then through, a quarter of revenue.

• Negative operating cash flow sustained over multiple years.

• Bonds redeeming bonds, refinancing disclosed in the notes themselves.

• A single dominant lender across loans, arranging and guarantees.

01.

A timeline the accounts already told

The receivership of Evaco Ltd, one of Mauritius's best-known luxury property developers, has been described in parts of the local press as a sudden shock to the sector. On the evidence of the company's own filings, it was not sudden at all.

For roughly ten consecutive quarters before joint receivers were appointed on 26 May 2026, the abridged accounts that Evaco published on the Stock Exchange of Mauritius traced a deteriorating path that was, in hindsight, difficult to misread: a shrinking top line, a widening cash deficit, a rising interest burden, and a capital structure increasingly dependent on refinancing rather than trading performance.

This piece reconstructs that path from the public record, sizes the exposure now facing the company's principal lender, and sets out what the episode implies for other developers, for creditors and buyers, for the regulators, and for a jurisdiction whose property model rests heavily on foreign capital.

It is an analysis of disclosed financial information, not an adjudication of conduct; questions of governance and oversight that have been raised elsewhere are matters for the receivers, the regulators and, where relevant, the courts.

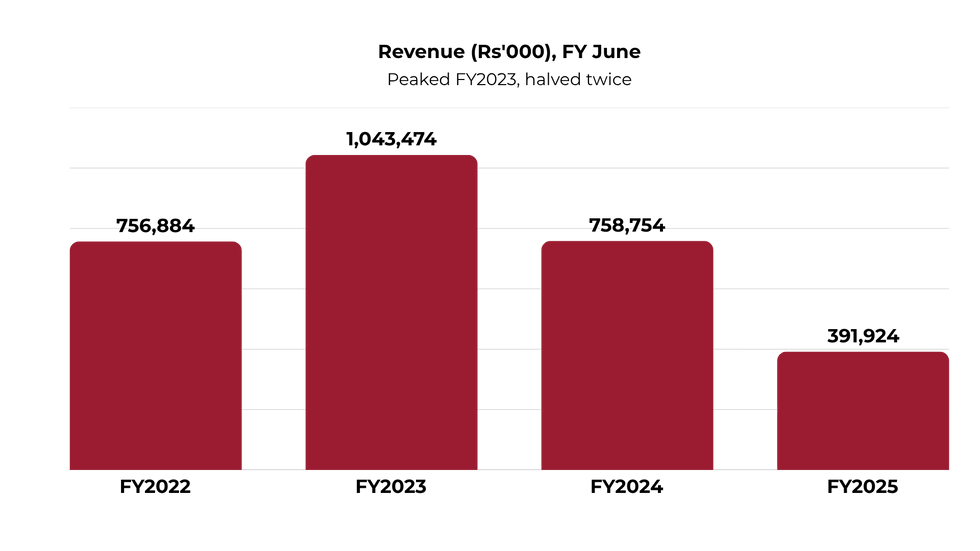

Across FY2022 to FY2025, consolidated revenue peaked in FY2023 at roughly Rs 1.04bn. It then fell to about Rs 759m in FY2024 and to Rs 392m in FY2025.

The interim filings show the same trajectory with greater granularity. On a like-for-like nine-month basis to 31 March, revenue moved from Rs 700m (FY2023) to Rs 557m, Rs 305m and finally Rs 216m by March 2026. The first-quarter figures are starker still: Rs 241m in the quarter to September 2023 became Rs 108m a year later and Rs 42m by September 2025.

Management attributed the shortfall consistently and, for the most part, to external causes: administrative delays in the processing of title deeds (a step that, in the company's telling, lengthened from roughly one month to six), a domestic labour shortage, foreign-currency scarcity in the banking system, construction-cost inflation, and supply-chain disruption.

Each interim report carried a recurring assurance that the deferred revenue would be recognised “in the upcoming quarters.” It was a forecast the subsequent filing repeatedly did not bear out.

The persistence of that pattern, i.e., adverse outcomes attributed to temporary, external factors, paired with forward revenue that kept slipping, is itself one of the more reliable qualitative markers of strain.

02.

Profit without cash

The single most important point for any reader of these accounts is that reported profit and underlying cash generation moved in opposite directions, and had done so for years.

Operating cash flow at the Group was negative in FY2022, FY2023, and FY2024, a cumulative operating outflow of roughly Rs 1.3bn over those three years. The period-end net cash position, presented net of bank overdraft as the company reports it, was negative throughout the record and deepened steadily: from about (Rs 401m) at June 2022 to (Rs 608m), (Rs 819m) and (Rs 978m) by June 2025.

FY2025 is the year most likely to mislead a casual reader. Evaco reported pre-tax profit of about Rs 134m, its strongest headline result in the window. Yet management's own commentary attributes that result to the revaluation of investment property, and the nine-month figures to March 2025 show an operating loss of around Rs 28m.

The profit, in other words, was a non-cash fair-value mark, not the product of trading. Strip the revaluation, and FY2025 operations were loss-making, consistent with interim filings that year.

The mechanism is straightforward. Costs are capitalised into work-in-progress and inventory, which sat between roughly Rs 1.8bn and Rs 3.0bn throughout, and on the face of it, into periodic revaluations, both of which can support an earnings line and a growing balance sheet even as cash drains away.

Total assets rose toward Rs 4.9bn while revenue fell, an expansion driven by capitalised development cost and asset marks rather than realised sales. The balance sheet inflated as the trading performance deflated.

The profit is made in the fourth quarter

This pattern is not only an annual one; it is visible quarter by quarter, and it is the clearest single piece of evidence in the record.

Evaco does not report its fourth quarter April to June on its own. That period can only be derived, as the difference between the audited full year and the nine-month interim that precedes it. Doing so is revealing. In FY2025 the group ran a pre-tax loss of about Rs 88m across its first nine operating months, then recognised a positive Rs 222m in that final, audit-time quarter to finish the year at a reported profit of Rs 134m.

Group pre-tax profit by window (Rs'000):

Group pre-tax profit (Rs'000) | FY2023 | FY2024 | FY2025 |

Nine months to 31 Mar (operating) | 96,053 | (31,614) | (88,245) |

Full year to 30 June (reported) | 106,641 | 31,526 | 133,981 |

Implied Q4, Apr-Jun | 10,588 | 63,140 | 222,226 |

The implied fourth quarter is the audited full year less the nine-month interim; it is not separately reported.

The full-year profit line and the interim windows are telling opposite stories, and the gap between them is non-cash.

This is the mechanism behind the divergence between profit and cash, now visible quarter by quarter rather than merely asserted. The interim windows are reported before the year-end revaluation of investment property; the annual figure is struck after it, and the sign of the result flips at the audit.

The reliance did not stabilise but grew: the implied fourth-quarter uplift rose from roughly Rs 11m in FY2023 to Rs 63m in FY2024 and Rs 222m in FY2025. As the operating business weakened, the company leaned ever more heavily on a non-cash mark to keep the headline in profit.

One qualification is warranted. The implied fourth-quarter figure absorbs any adjustment taken at the year-end, provisions, true-ups and the small discontinued-operations effect recognised in FY2025, not the revaluation alone. But its scale, and management's own attribution of the full-year result to the revaluation of investment property, leave little doubt as to the principal driver.

Group financial summary, as filed (Rs'000):

Year to 30 June | FY2022 | FY2023 | FY2024 | FY2025 |

Revenue | 756,884 | 1,043,474 | 758,754 | 391,924 |

Operating profit | 97,163 | 175,907 | 108,536 | 237,103 |

Finance costs | (57,008) | (69,266) | (77,010) | (103,122) |

Profit before tax | 40,155 | 106,641 | 31,526 | 133,981 |

Operating cash flow | (349,057) | (540,186) | (419,409) | 462,456 |

Net cash, period-end | (400,891) | (607,652) | (818,821) | (977,525) |

Total liabilities | 2,161,898 | 2,995,716 | 3,618,773 | 4,109,078 |

Total equity | 510,993 | 604,978 | 635,223 | 763,998 |

Operating profit and FY2025 pre-tax profit are materially affected by investment-property revaluation. FY2025 operating cash flow turning positive could be on the back of working-capital and/or customer-deposit movements, while investing outflows of about Rs 1.1bn left the year's net cash change negative. Pre-tax profit shown as operating profit plus finance costs.

03.

The cost of carry, and the refinancing treadmill

As revenue fell, the fixed cost of debt did not. Finance costs rose from about Rs 69m in FY2023 to Rs 77m in FY2024 and Rs 103m in FY2025. Measured against revenue, the burden moved from 6.6% to 10.1% to 26.3% across those three years, and on the nine-month figures to March 2026 reached roughly 40%.

By the final reporting period, interest was consuming around two-fifths of every rupee of revenue, set against an operating loss. On the operations alone, that is, before the revaluation that flatters the FY2025 headline, interest cover had effectively gone.

How the debt was serviced is disclosed in the accounts themselves, and it points to a refinancing dynamic rather than a deleveraging one. Evaco issued Rs 650m of redeemable notes in 2019, the proceeds of which were used in part to redeem earlier loan notes. Those 2019 notes matured in November 2024 and were refinanced through a fresh Rs 650m five-year note arranged with SBM Capital Markets.

In April 2025 the company listed two further tranches under an existing MUR 1.075bn note programme – MUR 393m and USD 5.653m of secured fixed-rate notes. The structure, on its own disclosures, was being rolled forward; new issuance was retiring maturing debt as much as funding new development.

A refinancing model of this kind functions only while the next round of funding is available. When the credit was withdrawn, the structure had no other source of liquidity to fall back on. The proximate trigger, according to local press accounts, was a demand on 25 May 2026 by Silver Bank, itself under receivership, for immediate repayment of roughly Rs 39.7m. A failing bank's recall of facilities pushed a far larger borrower into receivership the following day. The size of that final demand, set against the scale of the group, underlines the point: this was a liquidity failure waiting for a trigger, not a business felled by a single Rs 40m claim.

04.

Measuring the exposure to SBM

For the financial system, the most material question is what the receivership means for the State Bank of Mauritius, the group's principal banking partner. The exposure has three distinct components, and they carry very different risk characteristics.

The components

First, direct lending. SBM has acknowledged publicly, through the local press, that it initiated its own receivership step in respect of a claim of around Rs 2.4bn, and reports put its total credit exposure to Evaco at roughly Rs 2.4-2.5bn. SBM has said the decision to place the company in receivership followed a rigorous assessment process rather than an impulsive reaction. Second, a completion guarantee. Press reporting describes an additional SBM exposure of about Rs 2bn arising from a financial completion guarantee (garantie financière d'achèvement, or GFA) under which the bank may be obliged to complete the flagship Cap Marina development if the developer cannot. Third, an arranging and agency role: SBM Capital Markets arranged the listed notes and an SBM entity acts as paying agent and registrar, with the notes secured on a share pledge over a subsidiary and a first charge on the group's headquarters. This third strand is operational and reputational rather than principal credit risk, because the notes are held by external investors.

Sizing it against the bank's capital

The credit question is not the gross figure but the loss after recovery, and how that loss sits against SBM's capacity to absorb it. At the group level the buffer is substantial. SBM Holdings reported shareholders' equity of about MUR 38.5bn at 30 June 2025 on total assets of roughly MUR 446bn. Its capital adequacy ratio stood at about 20.5% and its Tier 1 ratio at 14.7%, comfortably above regulatory minimums, though its gross impaired-advances ratio had edged up to 8.7%. Against that capital base, even the full combined exposure of around Rs 4.5bn is on the order of a tenth of group equity, within, at the consolidated level, the kind of single-counterparty ceiling that a credit-concentration framework contemplates.

Why the GFA is the part to watch

The direct lending, on these numbers, is an earnings event for SBM rather than a capital event: a loss of one to three billion rupees would absorb a meaningful slice of a year's profit but would not threaten a bank with a 20%-plus capital ratio. The completion guarantee is more complex, and more interesting, because it converts the bank from creditor into developer of last resort. If the GFA crystallises, SBM is not simply writing off a loan; it must fund the completion of Cap Marina, while managing the contractual position of several hundred existing buyers. That is a combination of fresh liquidity commitment, construction-execution risk, and reputational exposure layered on top of the original credit loss. The headline number understates the operational complexity; the capital number overstates the comfort.

05.

The systemic map

Beyond the single-name exposure, the episode connects several nodes of the domestic system in ways worth setting out plainly.

Counterparty concentration

The most striking structural feature is how much of Evaco's capital structure ran through one systemically important, partly state-owned institution – as lender, as bond arranger, as paying agent, and as completion guarantor simultaneously. Concentration of that kind is not improper, but it removes the diversification of judgement that comes from multiple independent financiers, and it concentrates the consequences of a single credit decision. It is the clearest supervisory talking point in the file: how single-name and connected-role exposures are measured, aggregated, and stress-tested across a banking group.

Bank-to-borrower contagion

The trigger creditor, Silver Bank, was itself in receivership. A distressed bank liquidating its loan book toppled a borrower, a small but clean illustration of how stress propagates through a financial system rather than staying contained within one institution. It is also a reminder that a borrower's risk includes the health of its lenders, not only its own.

Public money

The Mauritius Investment Corporation (MIC) is reported to have disbursed Rs 100m to Evaco in October 2024, intended to support a commercial centre within the Cap Marina development, at a point when the group was already under financial strain. That capital now sits within the receivership pool, which raises legitimate questions about the due-diligence standard applied when public funds are deployed into an entity whose published cash position had been negative for years.

Confidence in listed debt

Four classes of secured, SEM-listed notes are now suspended from trading. Recovery for noteholders turns on the pledged security, a share pledge over a subsidiary and a first charge on the group's headquarters, tested against any competing bank claims in the priority waterfall. This is a domestic credit event on a market that has relatively few of them, and it will reasonably prompt closer scrutiny of property-backed corporate notes and, in time, wider spreads on comparable paper. The word “secured” in a listing particulars document is only as good as the realisable value and the priority of the security behind it.

06.

The jurisdiction

Mauritius has built a significant share of its inward investment story on residential schemes designed for foreign buyers – the IRS, PDS, RES, and Smart City structures – and luxury property has been promoted as a pillar of the island's foreign-direct-investment proposition.

Cap Marina alone comprises some 337 units sold at an average of around Rs 30m, roughly 70% of them pre-sold largely to South African and French buyers, against lifetime group sales reported at about Rs 12bn. A high-profile developer entering receivership with units undelivered is therefore not only a corporate event; it is a test of the credibility of the model itself.

Two features of that model now come into focus. The first is the asymmetry of protection. The completion guarantee that may rescue Cap Marina's foreign buyers is a feature of the schemes aimed at non-citizens; domestic buyers purchasing off-plan under ordinary arrangements generally enjoy no equivalent backstop. A failure of this kind exposes that gap and invites a policy debate about parity of protection. The second is reputational transmission: foreign buyers who experience delivery failure, or who watch the resolution process closely, recalibrate their view of jurisdiction risk, and that recalibration is slow to reverse. The damage, if it occurs, is to the perceived reliability of the framework, not to any single project.

The asset at risk here is not only a development at Cap-Malheureux. It is the confidence of the foreign capital on which a model depends.

07.

What developers should be watching in their own accounts

For other developers, the value of this episode is diagnostic. The signals that preceded Evaco's receivership are observable in any developer's own management accounts, well before they become public, and most are simple ratios rather than sophisticated models.

The following is a practical self-assessment, not a verdict on any particular firm.

• Operating cash flow vs profit. If profit is positive while operating cash flow is persistently negative, the profit is in the balance sheet, not the bank.

• Finance cost to revenue. Above 15% is a warning; approaching 25% on a falling top line is structural.

• Revaluation share of profit. Know how much of the earnings line is fair-value marks rather than realised margin.

• Interim vs annual divergence. If cumulative interim losses are reversed by a positive full-year result, the profit is being made in the unreported final quarter, typically a year-end revaluation. Compare the nine-month run to the audited year.

• Net cash trajectory. A deficit that deepens every period is the single hardest signal to argue with.

• Maturity wall vs sales pipeline. Map debt maturities against contracted, deliverable cash, not against forecast sales.

• Refinancing dependence. If new issuance is retiring old debt rather than funding build, model the day the market closes.

• Lender concentration. A single financier across loans, bonds, and guarantees is a single point of failure.

• Title and approval lead times. If recognition keeps slipping a quarter, treat the pipeline as deferred, not assured.

The practical defences follow directly: hold a genuine liquidity buffer rather than relying on the next refinancing; diversify funding sources and counterparties; stagger maturities so no single year carries a cliff; and report internally on cash conversion, not only on accounting profit. None of these is novel. The discipline is in applying them.

08.

What stakeholders can do now

The measures that follow are framed by stakeholder. They are risk-mitigation principles drawn from the structure of this case, not advice on Evaco specifically, whose affairs are now in the hands of the appointed receivers.

Lenders & banks

• Aggregate exposure across all roles – lending, arranging, agency, and guarantees – to a single name or group, not by product silo.

• Stress-test contingent guarantees (GFA and similar) for the cost of completion and the liquidity call.

• Re-underwrite property exposures on cash conversion and pre-sale quality, discounting revaluation-driven equity.

• Tighten covenants to cash-flow and liquidity tests, with earlier intervention triggers than payment default.

Regulators

• Review single-counterparty and connected-role concentration in property lending across systemically important banks.

• Consider parity of completion protection between foreign-scheme and domestic off-plan buyers.

• Strengthen continuous-disclosure expectations so cash and liquidity stress is as visible as reported profit.

• Coordinate resolution communication to protect jurisdiction credibility, not only individual creditors.

Bondholders & investors

• Test the realisable value and legal priority of “secured” collateral before relying on the label.

• Engage early and collectively through the noteholders' representative; understand the waterfall.

• Read interim filings for cash and finance-cost trends, not only the profit line and the narrative.

• Price property-backed paper for refinancing risk where issuance has been rolling debt forward.

Buyers & the public purse

• Foreign buyers: confirm whether a GFA exists, who stands behind it, and what it actually covers.

• Domestic off-plan buyers: seek escrow or staged-payment protection given the absence of a statutory backstop.

• Public investors (e.g. MIC): apply going-concern and cash-flow due diligence proportionate to the disclosed strain.

• All buyers: track delivery milestones against contract and document slippage in real time.

09.

Conclusion

The through-line of the Evaco file is not fraud or a sudden market reversal; it is the slow, legible accumulation of liquidity stress beneath an earnings line supported by fair-value accounting and a funding line supported by serial refinancing – until a single lender declined to roll the debt forward. Almost every element of that story was present in filings available to anyone who chose to read them. The gap that matters is the one between data that was available and data that was acted upon.

That gap is the practical lesson for every party here. For developers, it is a reason to manage to cash. For lenders and regulators, it is a reason to aggregate exposure and to weight liquidity as heavily as reported profit. For a jurisdiction whose property model runs on foreign confidence, it is a reason to treat the orderliness and transparency of this resolution as an asset in its own right. The receivership is now a recovery problem to be worked through by the appointed receivers. The systemic question - whether the warnings will be read earlier next time – remains open.

----

Methodology & sources

Financial figures are drawn from Evaco Ltd's abridged consolidated financial statements as filed on the Stock Exchange of Mauritius, covering FY2022 (audited) through the nine months to 31 March 2026 (unaudited). Interim periods are unaudited and figures are stated as filed. Corporate-action detail is taken from the SEM official notices and the receivers' notice of 28 May 2026. SBM Holdings capital figures are from its FY2025 reporting. Exposure figures attributed to SBM, the completion guarantee and the Mauritius Investment Corporation are reported in the local press (l'express, Le Défi, Le Mauricien, Scoop) and are labelled as such; they have not been independently audited here. This article is financial analysis and commentary, not investment, legal or accounting advice, and it does not adjudicate any question of conduct.

Comments